Cost of Long-term Care Survey

By Susan Suben

For the past 15 years, Genworth’s company, CareScout, has conducted surveys whose findings try to help individuals plan for long-term care. Genworth just released its 2018 Cost of Care Survey.

For the past 15 years, Genworth’s company, CareScout, has conducted surveys whose findings try to help individuals plan for long-term care. Genworth just released its 2018 Cost of Care Survey.

The survey includes the median cost of care around the country for nursing homes, assisted living facilities, adult day care, home health aides and homemaker services along with the increase in cost since 2017 and the five-year annual growth rate.

If you are in the process of planning for retirement and would like to include a strategy to protect yourself from the financial consequences of a LTC illness, this is an excellent source of information that includes an interactive map for each state.

CareScout contacted more than 49,000 providers to complete over 15,500 surveys. Below are basic definitions of facilities and services discussed in the survey. It is important to note that each state may categorize facilities/services differently and so might LTC insurance policies.

Nursing homes. They provide the highest levels of supervised skilled care, 24/7. Services include room and board, rehabilitation, medication management and personal care for individuals with functional or cognitive limitations.

Nursing homes. They provide the highest levels of supervised skilled care, 24/7. Services include room and board, rehabilitation, medication management and personal care for individuals with functional or cognitive limitations.

Assisted living facilities. They provide care in a residential type community. Communal meals, activities, personal care and medication management are included. Oftentimes, assisted living facilities offer a better quality of life alternative to a nursing home. Individuals with functional or cognitive needs can be accommodated but certain restrictions may apply based on the facility’s license.

Adult day care centers. They can conform to a social or medical model. The centers provide a safe environment for participants that promote socialization through communal meals and planned activities. Some programs also provide medication management and transportation and can cater to individuals with a cognitive impairment. Even though it is a very cost-effective community service, it is generally under-utilized by individuals needing LTC.

Home health aides. They can be certified, licensed or trained. Aides can work for Medicare-approved or non-approved agencies and provide personal care but not skilled care.

Homemaker services. They are designed to help individuals remain at home in a safe environment. Services can include laundry, cooking, cleaning, transportation and running errands. One of the chief benefits of homemaker services is the companionship provided to someone who is disabled.

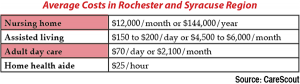

Currently in the Rochester and Syracuse region, the average nursing home costs approximately $12,000/month or $144,000/year; assisted living ranges from $150 to $200/day or $4500 to $6000/month; adult day care is approximately $70/day or $2100/month; a home health aide costs about $25/hour.

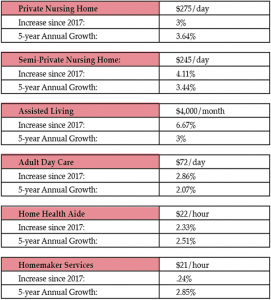

According to the Genworth’s 2018 Cost of Care findings, these are the national median daily rates for nursing homes, assisted living facilities, adult day care centers, home health aides and homemaker services along with the change since 2017 and the five-year annual growth.

What does all this mean to you? If you are thinking of purchasing LTC coverage, this information can help you select the best inflation protection for your needs. It will also help you determine what daily benefit to select in relationship to how much of the risk you would like to assume out-of-pocket and where you will be residing in retirement.

What does all this mean to you? If you are thinking of purchasing LTC coverage, this information can help you select the best inflation protection for your needs. It will also help you determine what daily benefit to select in relationship to how much of the risk you would like to assume out-of-pocket and where you will be residing in retirement.

Today, the most popular inflation protection selected by individuals designing a LTC policy is 3 percent compound. If you look at the five-year annual growth rates, they are 2.07 percent to 3.64 percent. A policy with 3 percent compound should be adequate.

The findings also show that assisted living is probably in greatest demand. The change in cost since 2017 is the highest of all the services 6.67 percent. This might encourage you to select more robust benefits for this LTC setting.

Trying to insure for nursing home costs, especially in the Rochester-Syracuse region, is very difficult because of how it impacts a LTC premium. Claims history supports the fact that most individuals want to stay at home or enter assisted living if they become ill. Designing your policy around the cost of home care and assisted living is a good approach, especially if most of your assets are in qualified funds (IRA, pension, 401K). Once you are taking the required minimum distribution, the funds are no longer considered an asset and therefore not susceptible to a Medicaid spend-down.

Utilizing the information found in the yearly Genworth Cost of Care survey is invaluable as you plan for LTC in retirement. This expense cannot be overlooked but it can be managed in a cost-effective way.

Susan Suben, MS, CSA, is president of Long Term Care Associates, Inc. and Elder Care Planning. She is a consultant for Canandaigua National Bank & Trust Company. She can be reached at 800-422-2655 or by email at susansuben@31greenbush.com.