No LTC Plan? What To Expect From Medica…

By Susan Suben

Each year we spend a great deal of time planning and budgeting for our vacation, our grandchildren’s college fund, our taxes, etc. If you’ve been reading my columns, you’ve heard me repeatedly say how important it is to plan for long-term care (LTC). But I bet many of you still haven’t done that. So what happens if you don’t have a LTC plan? Most people will spend down their retirement savings and go on Medicaid. A plan you never thought you would depend on.

Here are some facts to ponder. On average, a 65-year-old male can live to 86.6 years of age and a female to 88.8. Seventy percent of individuals over the age of 65 will need some type of LTC services. The No. 1 risk to your quality of life, independence, standard of living, asset preservation and legacy is a LTC illness.

Right now, the average cost of nursing home care in the Rochester area is $12,000 per month; assisted living, $5000 per month, and home care $25 an hour. How long will your assets last?

You do have many planning strategies to choose from to avoid going on Medicaid. They can include LTC insurance, life insurance with a LTC component, repositioning of assets or an irrevocable trust. But for the purpose of this article, let’s assume that you haven’t done any planning at all.

What can you expect if you have to go on Medicaid?

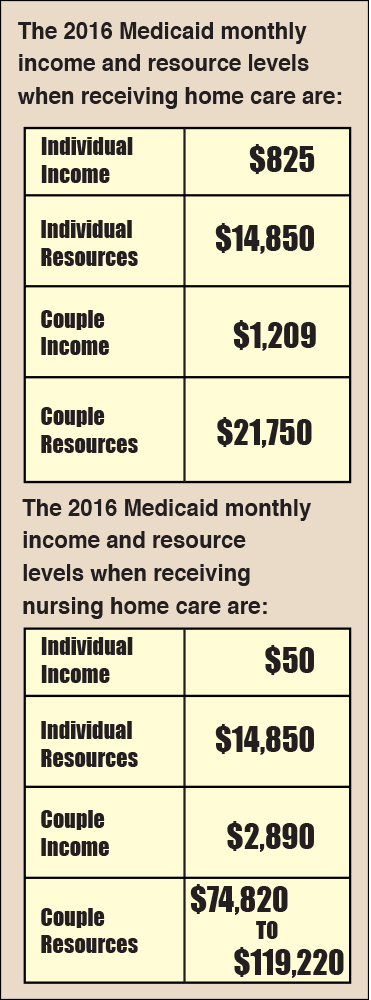

Medicaid is the “payer of last resort.” It is a federal/state program primarily designed to pay for nursing home care. It pays for limited home care. Very few assisted living facilities accept Medicaid. It is a means_tested program that requires certain income and asset levels. It was created to help those who are impoverished but many middle class families are relying upon it to pay for their care.

Social security, pension payments, unearned dividends, disability payments, rental income and an inheritance are all considered sources of income.

Bank accounts, securities, cash value of life insurance, annuities and vacation homes are considered resources. There is a five-year look back period along with penalty periods for transferring assets. Medicaid looks back five years at all your bank and financial accounts and will question any transfer over $2,000.

You apply for Medicaid through the Department of Social Services (DSS) in the county that you reside. I completed my father’s Medicaid application in Cortland County. After months of gathering his financial information and providing descriptions about transactions DSS considered questionable, he was finally approved. Don’t throw anything out if you think Medicaid will be your LTC plan! It will make it much easier for your adult children or an attorney to complete your application. If you do go to an attorney, you can pay approximately $6,000.

Certain assets are considered exempt — a home (that is occupied by the Medicaid applicant or his/her spouse, the applicant’s child under 21, an applicant’s sibling who has lived there for one year with an equity interest, or a caregiver child who has lived there for two years prior to the applicant’s institutionalization), one automobile for the community spouse, pre-paid funeral expenses, and life insurance with a face value of less than $1,500.

An IRA is exempt if it is in payment status. It will not be considered an asset but rather income. However, Medicaid can require a higher required minimum distribution (RMD) than the IRS.

The basic transfer and penalty rules can be somewhat confusing. There is no five-year look back period for home care like there is for nursing home care. For any assets transferred within the five-year look back period, there is a penalty period. The penalty period starts to run when the applicant is in a nursing home, has assets no greater than $14,850 and the Medicaid application has been filed. The penalty period is determined by dividing the amount of the transfer by the Medicaid nursing home regional rate. The regional rate for Rochester in 2015 was $10,660. If, for example, an applicant transferred $106,600 within the five-year look back period, that amount would be divided by $10,660 which means the applicant would wait 10 months to be eligible for Medicaid.

I have often heard it said that applying for Medicaid can be a demeaning and frustrating experience probably because it goes against our natural inclination to be independent and self-reliant.

So while you’re sitting in the sun on that long-awaited vacation and relaxing with that pretty umbrella drink, think about all that you saved and sacrificed to get there. Don’t let the government take it away from you because you did not plan for long-term care.

Susan Suben, MS, CSA, is president of Long Term Care Associates, Inc. and Elder Care Planning, and a consultant for Canandaigua National Bank & Trust Company. She can be reached at 800-422-2655 or by email at susansuben@31greenbush.com.