Don’t Let Fear Guide Your Investment Strategy

By Laurie Haelen

What a difference a few months has made in the financial markets. As of this writing, the S&P 500 is approaching a 20% decline, which is often defined as the signal for bear market conditions.

Market pundits and friends alike are stoking the bad news fire until it becomes something close to an inferno, consuming every twig of good news in its path. Suddenly, fear becomes the motive to change something, anything, in your portfolio to make it easier to tolerate the volatility. Usually, when this happens, the only ones who benefit from your fear-induced actions are those who caused it in the first place.

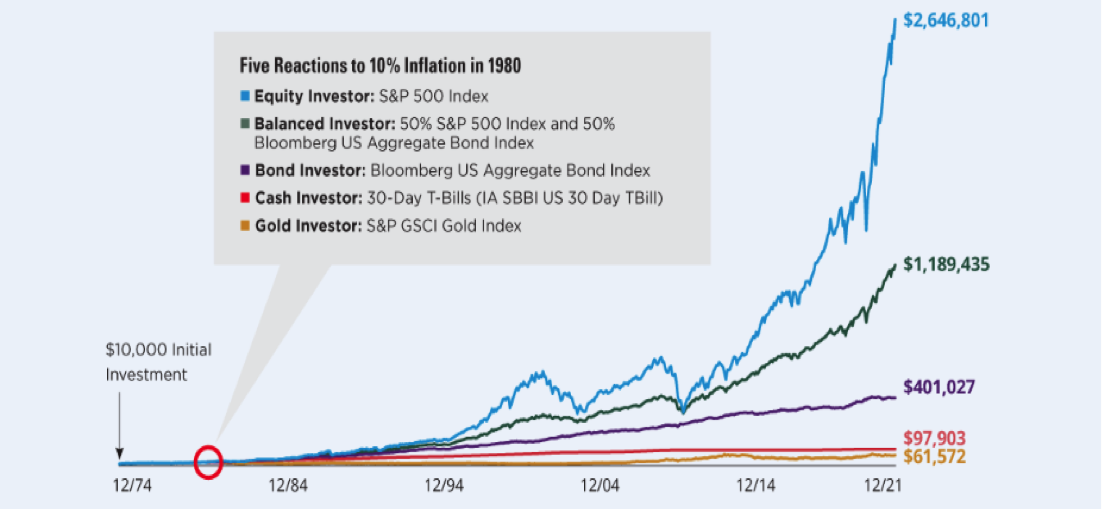

You see, fear sells, and when we buy, we fan the flames for a while until they burn out and the next fear can be stoked. In plainer terms, an example would be the last time we had high inflation, which was back in the ’80s. Inflation exceeded 10%, and volatility in the markets caused the same concerns that we see in the headlines today. At the time, it would have been hard to see that staying the course with stocks would be the best way to beat inflation over the next several decades. But the included chart shows the results for various asset classes since the last time inflation reared its ugly head.

The chart clearly shows that those who invested based upon concerns related to the volatility at the time, namely cash and gold investors, experienced the lowest returns as inflation abated and time smoothed the volatility of markets, as it usually does. Even with the tech crash and the financial crisis, those with equity exposure still ended up better off than those without — even in shorter time frames. But if you are retired or nearing retirement, you may still be looking for something you can do to feel more secure to ensure your plan will last as long as you need it to. Here are a few tips to help avoid letting fear divert or even destroy your long-term plan.

1. Review your portfolio and rebalance if appropriate.

Remember that if you liked stocks back in 2021 when they were going up, you are buying them on sale today. Even bonds have declined due to rising interest rates, and there may be an opportunity to purchase some with higher yields. Lower prices on assets mean higher yields, which equal higher income.

2. Make some Budget cuts.

It is easier to enjoy making purchases or going on expensive trips as your portfolio is going up. Look at your spending and see if there are ways to cut back a bit while inflation is taking a bite out of your purchasing power.

3. Do a Roth IRA conversion.

Since the taxes on a Roth conversion are based on the gains on the investments you convert from a regular IRA to a Roth, you may be able to do a Roth conversion with much less tax consequences. Or convert a larger portion of your IRA at the same tax consequence. This could save you some money both now and in the future, since Roth IRA funds grow tax free. Your tax adviser can run the numbers to help you evaluate the benefits of the conversion.

4. Consider doing some tax loss harvesting.

Many investors were shocked by capital gains — and the tax bills that came with them — after last year’s robust equity returns. This year, there may be opportunities to liquidate some holdings at a loss, either as part of the aforementioned portfolio rebalancing or as a single transaction in a taxable portfolio. Remember to be aware of the wash sale rules, which means you must be out of a specific position for more than 30 days to realize the loss on your tax return.

5. Revisit your financial plan.

There is a software program that can calculate the probability of the success of your overall financial plan in all types of markets. Either you, or ideally a certified financial planner professional, could run some different scenarios to see the impact of a bad market year (or more than one) on your portfolio and your plan. If your current allocation works well in most of these scenarios, you are probably OK, even if you don’t enjoy the fluctuations. In some cases, you may even be able to reduce your risk and still have the plan work, hence allowing you to sleep better at night.

These are a few tips that may help, but the most important thing is to not panic and not deviate from the plan you have without taking steps to ensure it still makes sense for you. Fear-mongering pundits like to sell you on the concept that “it’s different this time.” Even if it is, if you take steps to ensure you have the right financial plan in place, your outcome will be better, and you will hopefully be immune to the inevitable market gyrations that occur.